Recently, I was asked by directors of a regional bank for my perspective on China. I share it here as it may be of interest to our investors.

Given China’s scale it seems reasonable to call it at least an emerging super-power (second largest population; third largest landmass; second largest economy; etc.). We could quibble about timing, or the definition or role of a super-power but one can’t soberly deny China is just about to arrive at that status. (Our investors who have studied or traveled to China certainly come away with this sense.)

Yet, there is a consistent drumbeat from the West that China is second rate, does not deserve the mantle, is about to collapse, or can only be viewed as an adversary. This is rooted in misunderstanding, naivety, conceit and possibly racism. In addition to the scale elements listed above, China is an independent, sovereign nation with 5,000 years of recorded history. Certainly, it has the right to and authority for self-determination. That right, since 1949, has been manifest in a communist party dictatorship that espouses socialist/communist principles. Deng Xiaoping, after being purged three times, gained power after Mao’s death in the mid-1970s and set about opening China’s economy, which Mao had all but ruined. He coined his program the “Open Door Policy” and it is chiefly responsible for the economic success we’ve seen since.

Deng promoted capitalist methods in his policy using slogans like, and I paraphrase, “to get rich is glorious” and “who cares if a cat is black or white as long as it catches mice.” Historically, the Chinese have been pretty good at commerce. It turns out, once many of the obstacles Mao erected were cleared away by Deng, that they are still pretty good at it. Said in another way, by most accounts the Open Door Policy has brought China back to economic parity with much of the world.

To my knowledge, no country has lifted more people out of poverty in such a brief timeframe as China has, ever. Gone is the reputation China had when I was a child of being a poor, third world nation unable to feed itself, subject to natural and other disaster, and foreign humiliation. Granted, much of China’s earlier poverty, and backwardness, was self-inflicted, but in the last forty years China has caught up with and surpassed some once leading nations (Germany, Japan, etc.) economically, and in many other aspects.

I experienced the beginnings of the Open Door Policy from the ground, in China. Because of the Policy, in 1988 I, a foreign person in China, was legally able to establish a company. I started with one and grew to about 25,000 employees. For the first couple years I watched them come to their first job off the farm, learn industrial culture - how to dress, how to arrive at work on time, how to achieve high quality standards, how to take a break, how to work safely, how to receive and deposit a payroll check, and even how to accept income tax. Over the years they all became skilled, loyal and valued employees, and respectable middle-class citizens: paying taxes, buying motorcycles, then automobiles, mobile phones, enjoying eating out at restaurants, drinking imported wines, setting up retirement accounts, taking vacations both in and out of China and sending their children to good schools. I would say this result is very much like the American Dream, and in that regard I would say they are very much like Americans. I would add that the Chinese have a very strong work ethic, very similar to what was Americans’ in the 1950s: Get a good job, work hard, save some money and try to enjoy life. I also perceive that they feel about their government as many American’s do theirs – the system works, isn’t perfect, and offers prospects for a better future.

Deng’s genius in the Open Door Policy was not only to economically unshackle the average citizen, but also to utilize development methods already proven effective in other countries. China has emulated how Japan started (light industrial products for export); how the U.S. established its national interstate road system; and how Europe operates its massive port/shipping infrastructure, to name a few examples.

A micro example of the legacy of the Policy is the very business I mention above. Since opening in 1988 the business endures and excels. After thirty-four years of operation, competing with low-cost sources Vietnam, Indonesia and India, it is still, consistently, the best performer on a net margin basis. It makes world class, name-brand flagship products (highest difficulty and complexity) for one of the best brands in the world. China lost its low-cost advantage a decade ago, but our Chinese managers continue to innovate and find efficiencies to stay competitive and profitable. On top of this, thirty years ago we exported 100% of our China-sourced product. Today almost half of it stays in China for domestic consumption.

Many observers have misunderstood China’s economic success to mean it is now capitalist with a propensity to move toward democracy. Nothing could be further from the truth. They will permit capitalist activity as long as it is beneficial to the overall socialist cause. However, they will intervene when something is contrary to those principles. Witness recent central government intervention in several high-flying public companies because those businesses were deemed harmful to society; or public dressing down of several billionaires (Jack Ma of Alibaba for example) who thought they were above the law or untouchable because of their wealth. Here is where the mistaken observer claims China is veering off into the weeds, when in fact they are doing precisely as their principles dictate.

Undeniably, China has had some recent examples of questionable action internationally: totally abrogated their contractual pledge to leave Hong Kong alone for fifty years; ridiculous claims about offshore and territorial rights in and around the South China Sea; engaged in malicious cyber-attacks as well as industrial espionage particularly in the U.S. Domestically, there are also examples: unprecedented social control, market intervention, Xi Jinping’s declaration of emperor for life and his decision to align, for the time being, with Putin/Russia.

In all the years I’ve been a student of China (since 1975) there have been frequent predictions of China’s impending demise. I can’t predict the future, but I can say unequivocally those pundits have been wrong. (For some comparative context, as of this writing, China is sixty-three years into its national experiment. They are about where the U.S. was when Abraham Lincoln was in his second term in the Illinois House or Representatives. On that note, over its first sixty-three years and beyond, many predicted the impending collapse of the U.S.)

I do not pretend that China is some benign entity that should be ignored, or lightly treated. On the contrary, they should be engaged and deemed and treated as a partner. Those with experience know partnership means work, understanding, patience and give-and-take. In the not-too-distant past China demonstrated their willingness to be an able partner, as had the U.S. Recently though both sides have been very weak in this respect. I would like to see both sides re-double their efforts in the relationship and both sides up-hold their commitment to one another. National eccentricities can exist and not terminally impact a long-term relationship. The U.S. isn’t engaged in cyber-attacks and industrial espionage outside of the U.S.? And our own internal racial tensions should become a reason for terminating a national alliance?

Does China have the system, the structure, the institutions to innovate and sustain itself and perhaps lead and excel? Who knows. What I do know is China will do what is in China’s best interest, and they mean to compete using their system, not that of the West. I do believe China wishes to be part of the international community both behaving with high standards, and maintaining high standards of responsibility. If “containment” and isolation continue to be the West’s objective China will simply create other spheres of influence that are easier for them to operate and thrive in. We see evidence of this already. To continue down this road would be unfortunate, and un-necessary, and is avoidable.

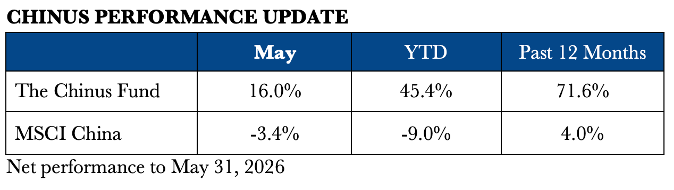

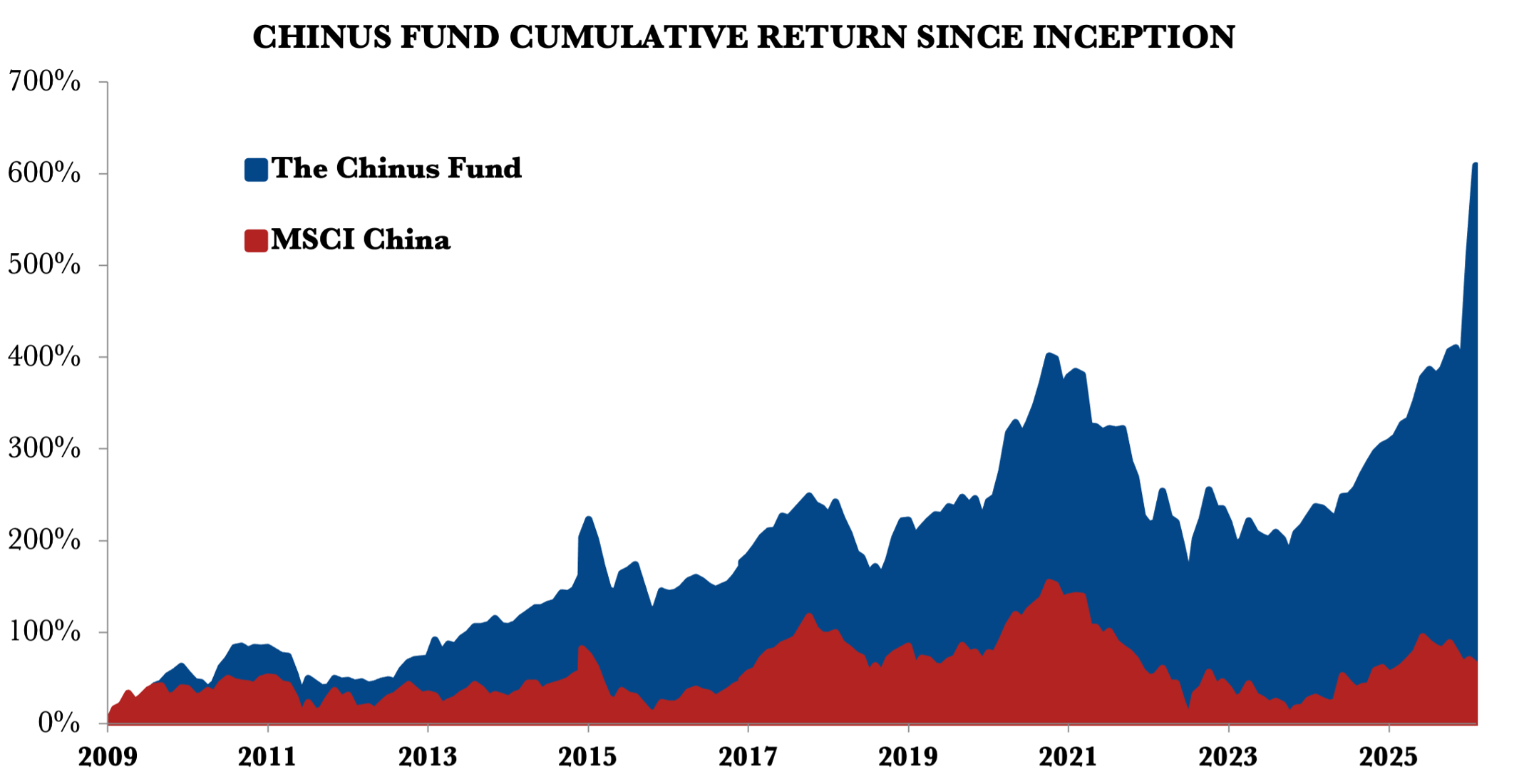

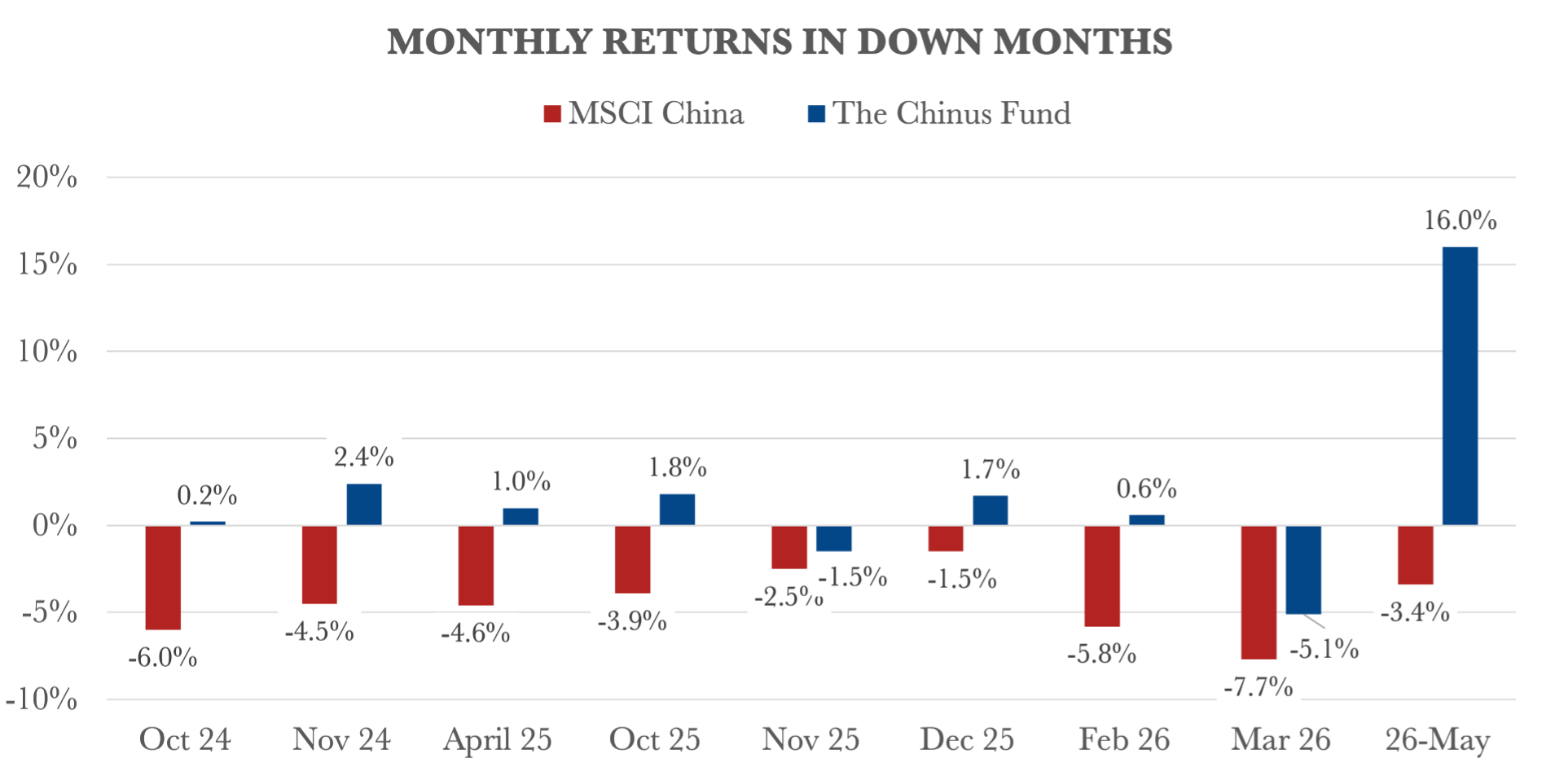

To conclude, surely China is now one of the top nations in the world and is here to stay. It should be recognized as a legitimate player that deserves and commands respect and should be dealt with on the basis of an equal, both as a competitor and a partner. Viewed from an un-informed perspective some of their policies and decisions look odd and sometimes extreme, and some are. On the other hand, those odd-looking policies and decisions are what’s best for China, and that’s all one should expect. The same is true for the U.S. and the West in general. It would be regrettable because of these and other differences to conclude that China is an enemy and they should be isolated or contained. They won’t be contained as there is no longer a hyper-power who could lead/achieve such containment. Despite its structural, political and social differences from the West, China’s economic expansion, in the long run, will continue. Charles and I believe, as we have from the onset, that our Chinus fund is well positioned to achieve superior gains there.