A Contrarian Case for India

/It would be easy to give up on India right now. Although the Modi government enacted one of the strictest lockdowns in the world, Covid-19 cases are rising rapidly. Tens of millions of migrant laborers fled from large cities and returned to their villages. Credit growth has stalled after several banks had to be taken over by the government in the past year. India’s economy is forecast to shrink by 5-10% this year.

In overcoming the pandemic, India has one distinct advantage over the rest of world. It experienced a similar short-term economic shock during demonetization in late 2016, when President Modi declared without advance notice that 86% of India’s cash was no longer valid. The Indian economy came to a standstill that lasted approximately three months before sufficient volumes of a new currency were produced. India was able to bounce back quickly following that economic shock, with GDP growth recovering to over 8% within a year. Indian companies, therefore, have experience in recovering from short-term economic shocks, which should aid India’s rebound this year.

India stocks, most of which were already in a severe multi-year bear market prior to the pandemic, experienced one of the steepest sell-offs globally in March. Foreign investors pulled $8.3 billion out of Indian markets, the highest monthly outflow since the financial crisis in 2008.

We have a contrarian view on India and believe it offers very attractive upside potential over the next three years. A closer examination of the market dynamics in India reveals a critical distinction - the market declines since 2018 have been largely sentiment-driven and not due to a corresponding decline in corporate profitability. As a result, valuations in India have declined significantly since the start of 2018 and now trade at the lowest level in over a decade.

Price to Book Valuations by Market Cap in India

It is important to note that the sentiment-driven market declines have been broad-based, impacting both strong and weak performing companies. This has caused companies in India with rising profits to experience massive valuation discounts.

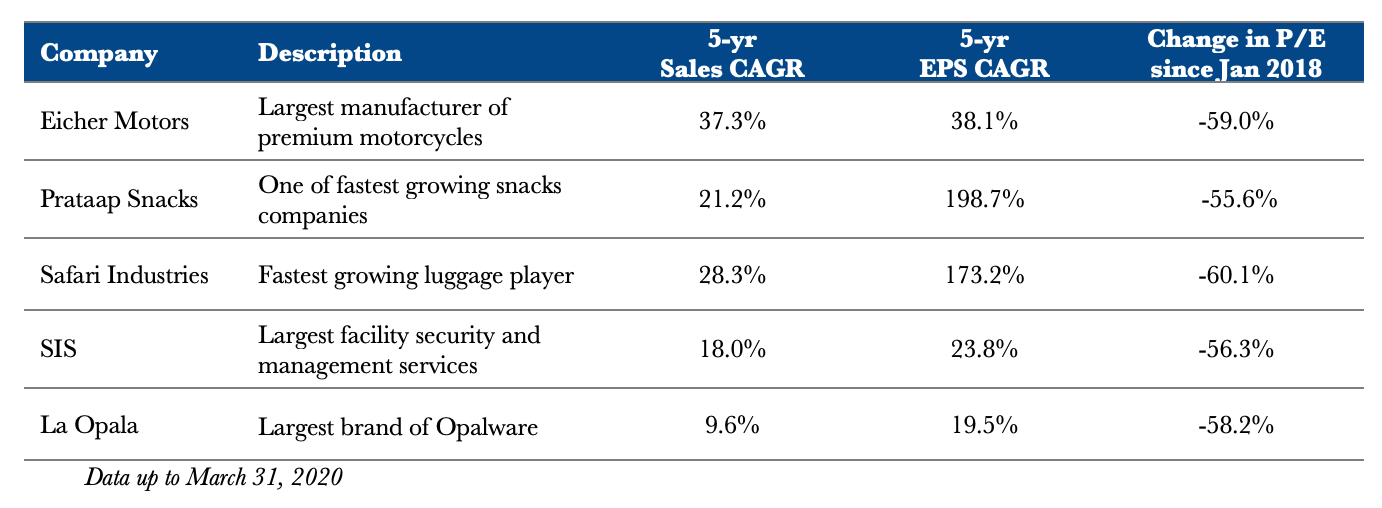

This divergence between corporate operating performance and stock performance has particularly impacted our managers in India, who focus on companies with rapidly growing profits. Indus Manager I-1’s top 10 positions, for example, generated average five-year revenue and earnings growth of 21%. Despite that stellar operating performance, those companies suffered a 56% decline in average trailing P/E ratio since the start of 2018. Some specific examples include:

Manager I-1’s performance, which historically has closely tracked its portfolio company profit growth, started lagging at the beginning of 2018, and the gap has widened significantly since then.

Indus Manager I-1 Trajectory of NAV vs. Portfolio Profits

From 2013 through 2017, when NAV tracked profits, Manager I-1 handily outperformed the MSCI India index every year, generating a 172% cumulative gain versus 42% for the index. Over the past two years, though, valuation compression caused Manager I-1 to underperform the market, generating a -32% return compared to a -3% for the index.

The large divergence between Manager I-1’s performance and portfolio profit growth since 2018 means that its portfolio now has substantial intrinsic value that is not reflected in the share price. There is very large potential upside, therefore, just from Manager I-1’s NAV catching up to its portfolio profits.

Manager I-1 conservatively forecasts that its portfolio companies will generate zero profit growth this year, and then 15% annual growth in 2021 and 2022. The combination of this modest profit growth and valuation normalization back to 2017 levels would cause a 381% jump in Manager’s I-1’s NAV. The other three Indus managers have similar upside potential.

There are additional potential gains if portfolio company profits rebound stronger than the 15% conservative forecast for 2021 and 2022. Indus managers’ portfolio companies are generally sector leaders with strong balance sheets, and these companies are expected to emerge from the pandemic with significantly higher market share and profit margins as weaker competitors are forced to exit the market.

For these reasons, we believe that our managers’ portfolios have the highest three-year upside potential that we have seen since launching the Indus Fund in 2010. This upside potential requires only that portfolio companies achieve modest profit growth and P/E multiples normalize back to 2017 levels.

Bajaj Finance best illustrates the opportunity that India offers now. Bajaj is the leading consumer finance company in India and is the Indus Fund’s largest aggregate position. Over the past 12 years prior to the lockdown, Bajaj grew revenue by 42% CAGR, profit by 62% CAGR, and its share price by over 45% CAGR. The cumulative gain in Bajaj’s share price over that period is over 8,500%.

Since the lockdown, Bajaj has been one of the hardest hit finance companies. Its share price declined by 16% in May and is now down approximately 60% since the start of the year. The sell-off is not due to any operational issues and is primarily sentiment driven. In fact, with one of the strongest balance sheets and most widely used fintech platforms (92% of customers make payments electronically), Bajaj will likely emerge from the lockdown with a significantly enhanced competitive position.

Bajaj’s share price has historically performed strongly after major crises. There have been two major corrections in Bajaj’s share price over the previous five years. The first happened after demonetization in late 2016 when Bajaj’s shares declined by 25% over two months. The second happened in 2018 when a blue-chip infrastructure bank, IL&FS, unexpectedly defaulted on its bonds, causing investors to exit out of finance stocks. After those sell-offs, Bajaj’s stock price averaged over 100% annual gains as its stock price caught up to its profit growth.

Bajaj’s stock price decline from the pandemic is significantly larger than the previous two crises, which provides more room to rebound. The market has started to recognize Bajaj’s large potential upside this month. Bajaj’s stock price jumped 38% MTD through June 19.

Indus Manager I-3 forecasts that Bajaj’s earnings will grow by 5x over the next five years. Bajaj currently trades at 16.5 PER FY2022. If its multiple increases to its historic average of 30x, Bajaj’s gain over the next five years would be approximately 10x. A 10x return over five years may sound outlandish, but in Bajaj’s case, it would be a letdown - it equates to 58% CAGR, which is substantially below Bajaj’s average annual returns following the past two crises.

That is not to say there are not substantial risks. India being India, the path back to normalcy will likely encounter numerous speed bumps. We have summarized some of the main risks here. For investors who have the fortitude to handle the volatility, our managers’ portfolios should generate extremely attractive returns over the next three years if India gets back to normal.

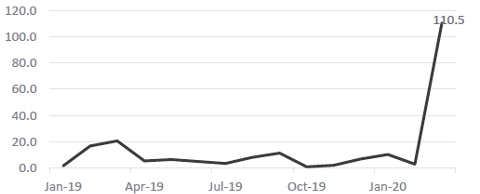

Corporate insiders in India share our view. Indian insiders (founders and management teams) dramatically increased their purchase of company shares in March.

Stock Purchases by Corporate Insiders Soared in March

Indus Manager I-3 reported to us this month (our bolding):

The stock charts and data above, almost scream that it is wise and pays handsomely to invest during such times. Nevertheless, it requires courage to remain non-consensus. It is hard to stand up to uncertainty, especially when we haven’t seen anything like this before. But that’s our test of character when pessimism reigns but opportunity shouts. It’s when all the near -term negativity is reflected in the prices. The long-term opportunity is magnified when markets extrapolate the near-term uncertainty, believing it to last forever and the crowd refuses to look at the basic structural issues which remain undented. Stock prices usually are at their lows then. They scream opportunity. That’s where the private sector financials appear to be at the moment – based on history, data and human behavior.

We agree with Manager I-3 that, contrary to current investor sentiment, India screams opportunity right now.