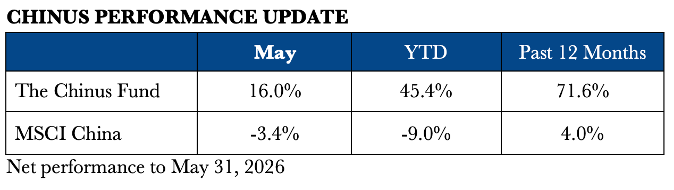

Building a More Resilient China Strategy: Chinus Performance Update

/Over the past three years, we have added three exceptional investment managers to the Chinus Fund. These additions have materially strengthened the Fund's return profile while improving its resilience during periods of market stress.

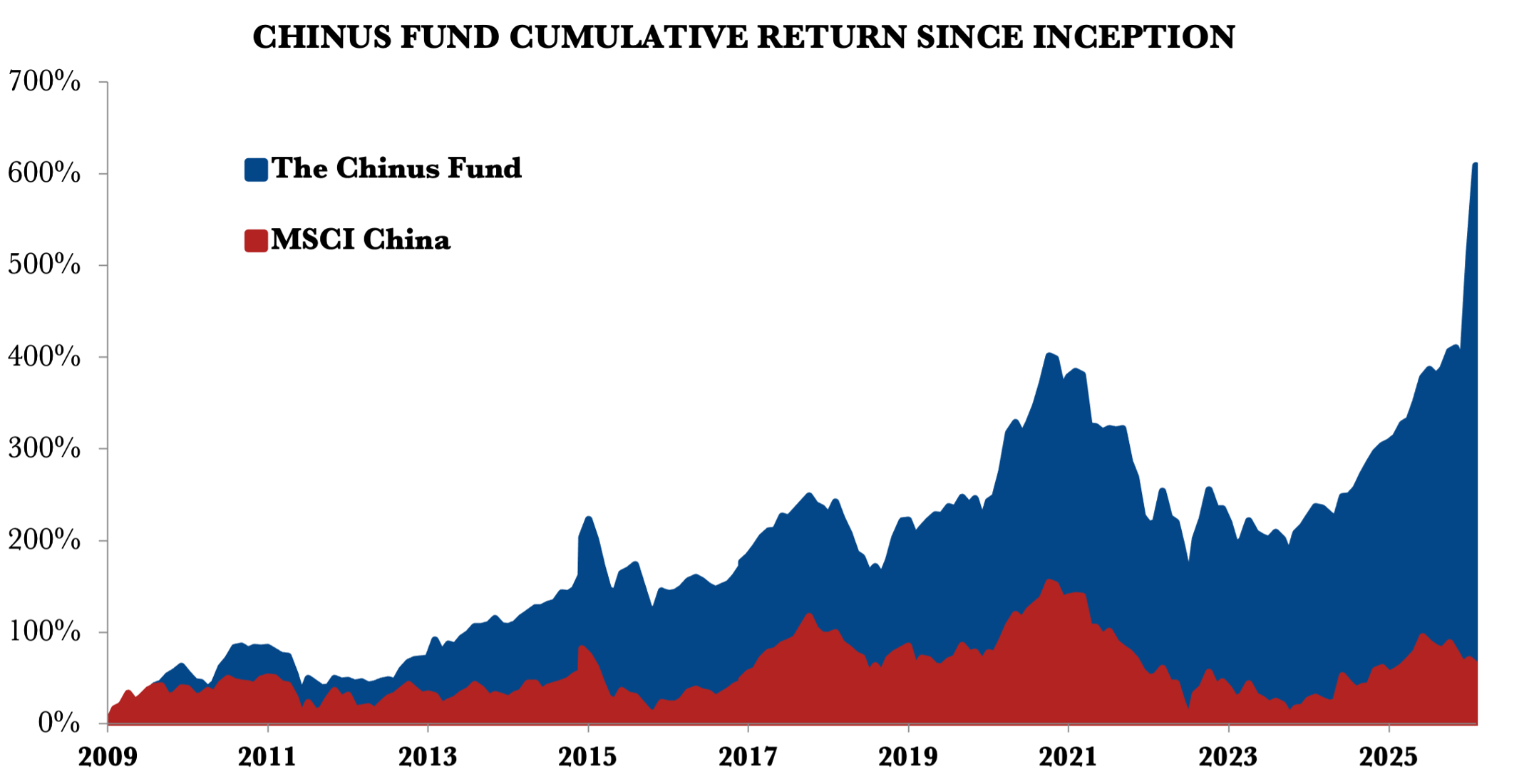

Two of these managers employ differentiated macro/micro investment strategies that combine top-down macroeconomic analysis with bottom-up security selection. Their long-term records have been exceptional. Since its inception in 2014, one manager has generated a cumulative return exceeding 7,700% (more than 40% annualized) during a period in which the broader Chinese equity market was essentially flat. The second manager has returned nearly 1,000% (27% annualized) since 2016. Both managers have experienced only one negative calendar year and generated positive returns throughout 2021–2023, when Chinese equities declined by nearly 50%.

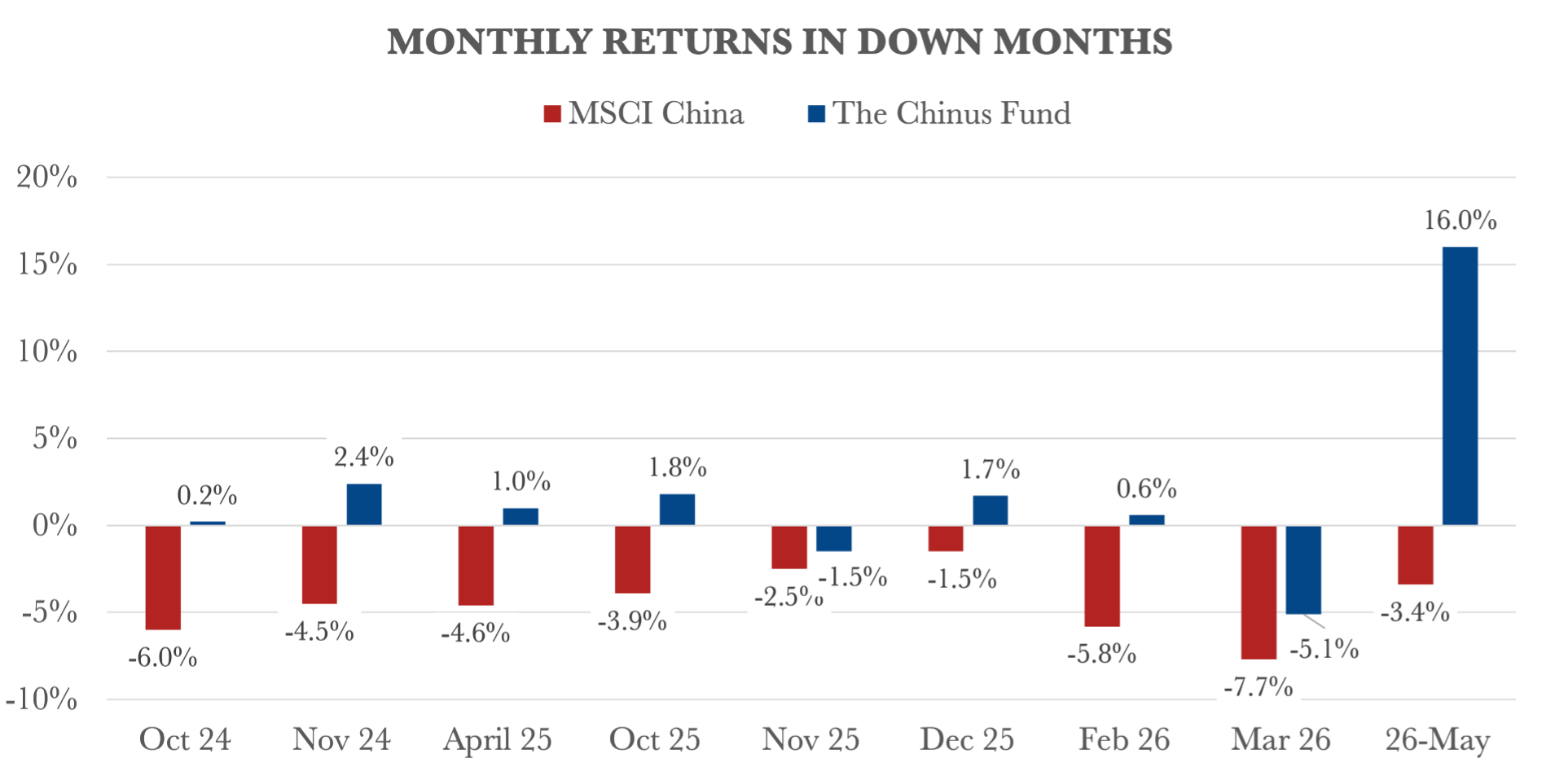

These additions have also significantly improved the Chinus Fund's downside characteristics. Over the past 19 months, the MSCI China Index recorded nine negative months, with an average decline of 4.4%. During those same periods, the Chinus Fund generated positive returns in seven of the nine months and produced an average gain of 1.9% across all nine down-market periods.

As a result, the Fund has delivered substantially stronger performance while reducing its dependence on market direction. The combination of fundamentally driven long/short managers with differentiated macro/micro strategies has created a more balanced portfolio capable of participating in rising markets while seeking to preserve capital during periods of heightened volatility.

As macroeconomic uncertainty continues to increase globally, we believe this diversified investment approach positions the Chinus Fund to generate attractive long-term returns and provide a differentiated source of alpha for institutional and high-net-worth investors.